2:45 To Doom-a

The stock and bond market have been strong lately, boosting returns of the funds in both Powerfund portfolios. If bonds were sinking and rates were climbing, we’d likely be shifting money from stocks to bonds at this time. In most cases, stocks, even at these levels, are still a better deal than bonds (although stocks remain the riskier asset class, bond bubble or no bond bubble).

Case in point: The recent sale of $1.1 billion in bonds by Johnson & Johnson (JNJ). Half of these were 10-year notes yielding 2.95%, the lowest yield for a 10-year bond offered by corporate America since at least 1981 – and likely for decades before that.

This by itself is interesting, but when you consider JNJ pays a dividend (currently taxed at a lower rate than bond interest) of around 3.4%, you have to wonder why investors would rather earn less in bonds than stocks.

Fear is the only answer. Sure the bond price may slip a little if rates climb, but if you hold the bond to maturity you are 99.9% sure to see your 2.95% payments along the way. But dividends at JNJ are more reliable than many other company’s bond payments. More importantly, they generally only go one way: up.

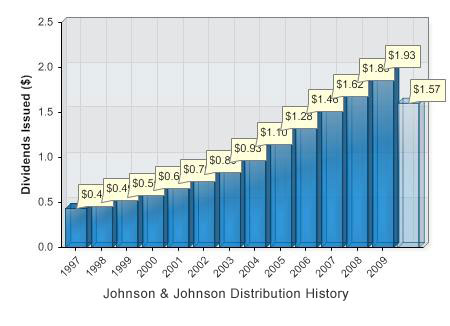

Ten years ago JNJ paid out $0.62 per share in dividends. This year they will probably pay $2.11 (they already paid out $1.57 thus far).

Granted JNJ is in the highest tier of credit ratings along with the US government, Exxon Mobil and Microsoft, but why lock in a fixed 2.95% when you can almost guarantee a 3.5% yield that will go up?

Downside. JNJ stock fell about 30% from the peak in August 2008 to the bottom March 2009. While that was less than the stock market, it’s a lot of money to lose in less than a year. Most bonds don’t do that, although junk bonds often do, and emerging market bonds, a big favorite now, sure can.

And it’s not like this last crash was the only crash since 1987. 50% drops in stocks seem to happen every few years now. This would be fine if stocks went up over time, but they now seem to be going nowhere. That’s left investors with the slow drag of professionals’ fees and bad ideas and the sharp pain of being much less wealthy than a few months ago – a sensation that is hard to stomach the closer retirement looms as it is for millions of baby boomers.

The icing on the cake strangely enough may have been the so-called ‘flash crash’ from May of this year. Also known as “The Crash of 2:45,” this massive but short lived drop in the market taught investors that stocks are about as stable as the Greek economy, with the ability to destroy a big chunk of your nest egg in seconds because of mysterious glitches or possibly sinister market manipulators and computers. No thanks, I’ll take bonds.

While this bond favoritism has led many experts to note the bond bubble building and to warn that you are about to get ‘killed’ in bonds, it is worth noting that this is nothing but a return to the way things have always been on Wall Street – until the nonsense of stock market hysteria in the late 1990s capped off a too-long bull market.

Through most of history, safe bonds yielded less than stocks. It was called the risk premium – which means the extra reward you expect for taking on higher risk. Sure stocks paid 7% dividends (imagine…), but they can crash 90% (it was hard to forget 1929 back then) and dividends can get cut. Just recently we saw dividends get cut across the S&P 500 by a larger percentage (thank you banks) than any time since the Depression.

What we are seeing is the return of the largely true opinion that stocks are a lot riskier than bonds and are not appropriate for large portions of a portfolio if you need a good part of your money in even the next 10 years. And at high enough stock prices, stock drops can take a lifetime to recover from. Those who bought an index of Japanese stocks in 1990 or U.S. tech stocks in 2000 will never see their original investment back adjusting for inflation in their entire lives in all likelihood (falling around 75% and 50% from peak respectively). Real estate is no better; those who bought homes in hot markets three years ago will probably never see the peak price adjusting for inflation.

That said, the real ‘new normal’ is stocks need to be cheaper than bonds even if in theory you can prove why the Dow is worth 36,000 and they are now cheaper.

This is a good thing for long-term investors and the young and those with higher risk tolerances because you will finally start earning more than everybody else in cash and bonds and real estate, just like the stock market was for most of the last 100 years.

There may be a bond bubble, but unlike the real estate bubble, tech stock bubble, tulip bulb bubble, beanie babies bubble, and now growing gold bubble, you won’t lose 80% of your money when it collapses. By the way, real estate investors using borrowed money typically lose 100%+ of “their money.”

You will lose, but it’s a loss you can sleep with. Very long-term investment grade bond investors could see some significant hits to bond prices, perhaps as high as 25% if and when longer-term rates go up, but most are investing in short and intermediate term bonds. Still, the JNJ stock investor is going to do better than the JNJ bond investor over the next 10 years unless we go into a deflationary death spiral, in which case I’m not sure how well stock or corporate bond investors are going to do. We’re not 100% stocks because we still expect to see chances to increase stock allocations at better times.

0 COMMENTS POST A COMMENT